As

of 6 April 2020, 96% of all world destinations have implemented travel

restrictions. About 90 destinations were completely or partially closed for

tourists, while another 44 destinations were reportedly closing their borders.

Apart from that, many airlines are now capping

their aircraft occupancy amid the pandemic. New seating patterns have been

designed with the middle seat left empty. To ensure social distancing for

passengers, some airlines such as Delta are blocking certain window and aisle

seats from being booked. This has further reduced capacity.

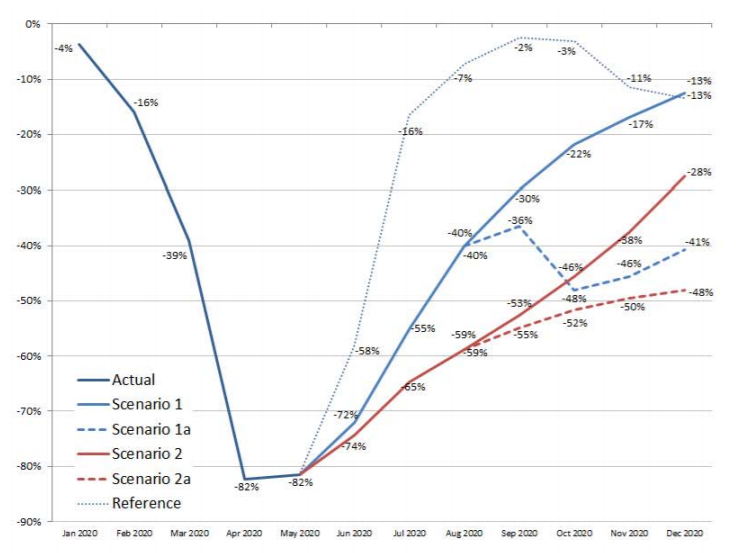

The

International Civil Aviation Organization (ICAO) has built a scenario to help

gauge potential economic implications of the Covid-19 pandemic. Scenarios are

not forecast. Given rapidly changing circumstances, these are merely indicative

of possible paths or consequential outcomes out of many.

Considering shapes of economic recession

and recovery, ICAO has developed four different recovery paths (“Nike swoosh”,

“W”, “U” and “L”) under two indicative scenarios: -

|

Baseline (counterfactual, no COVID-19

pandemic)

–

Originally

planned or business as usual: trend line growth from 2019 level

Scenario 1

– Path 1 (“Nike swoosh”-shaped): Smooth

capacity recovery to 80% of Baseline level by December with pent-up demand

–

Path

1a (W-shaped): Capacity to start with smooth recovery but then turn back down

due to over-capacity

Scenario 2

– Path 2 (U-shaped): Slow progression of

capacity recovery to 60%, picking up more demand in 4Q

– Path 2a (L-shaped): Recovery to 40% at

diminishing speed due to respite and continuous demand slump

Reference (V-shaped, based on the latest

airlines schedules)

–

Currently

planned: Weekly changes (some airlines have not yet filed 4Q schedules)

|

Seat

Capacity Change Compared to Baseline

Prior

to the outbreak, airlines had planned to increase seat capacity in 2020 by 3.5%,

compared to 2019. However according to ICAO’s estimation, seating capacity

could drop 40% to 53% below the Baseline level. Biggest capacity reduction is

expected to be in the Middle East.

World Total

Passenger Numbers Compared to Baseline & 2019

Under

the Baseline scenario, passenger demand could have increased 187 million for

2020 as compared to 2019, given the originally planned seat capacity. ICAO

projected that passenger demand could instead reduce from the Baseline by 2,247

million to 2,915 million, or 2,061 million to 2,728 million below the 2019

level. The most substantial demand reduction is expected to be in the

Asia/Pacific.

Passenger

Revenues Compared to Baseline

Without

Covid-19, airlines’ gross passenger operating revenues could have increased USD

22 billion for 2020, compared to 2019. However according to the latest

estimates, airlines’ revenue could instead slip USD 297 billion to 384 billion

below the Baseline. Approximately 60% of revenue loss would be recorded by

Asia/Pacific and Europe.

Recession

shape can always change given the uncertain outlook. How long will the pandemic

last? How severe it could affect the economy? How confident are travellers to

travel with airlines? How would business structure and consumer behaviours

change?

IATA

said (on 3rd June) that the unprecedented low traffic in April may have been

the bottom, as flights rose 30% in May from April, though still 73% below 1st

Jan. Meanwhile, business confidence has turned up in key economies – PMI

indices in China, US, Germany and Japan are rising. Global travel bookings have

also shown some improvement throughout May. All these are good signs for the

aviation sector as well as for the tourism industry.

Hopefully we have passed the inflexion point!

Reference:

1. Effects of Novel Coronavirus (COVID‐19) on Civil Aviation: Economic Impact

Analysis, 1 June 2020, ICAO

2. Covid-19: Air Travel Reaching a Turning

Point, 3 June 2020, IATA

No comments:

Post a Comment