Monday, 31 August 2020

Friday, 28 August 2020

A Boomerang Worth RM6.61 Billion?

The Minister of

Finance reported on Monday, 24 August 2020, that the PH Government had awarded

RM6.61 billion contracts (101 in number) by way of direct negotiations. This

was during the 22 months PH was in power. Is that true? And under what criteria

could a Government conduct direct negotiations?

The Ministry of

Finance (“MOF”) has five conditions for direct negotiations:

i.

Urgent

need;

ii.

Compatibility

issues;

iii.

One

supplier for product/service;

iv.

Security/strategic

importance; and

v.

Bumiputra

party has fulfilled all requirements

Perhaps, one

could add that if intellectual property rights or real property rights are

unique for the project; competitive process is too expensive; and, where competitive

process will fail to produce a satisfactory offer into the above list. (These

are conditions for consideration and not part of the MOF’s current criteria).

The term “direct

negotiations” refers to exclusive dealings between an agency of the Government

and a counterparty without undergoing a competitive process. The closed nature

of direct negotiations can create opportunities for dishonest (or partial

conduct) with allegations (or perceptions) of corrupt conduct. Measures could

be taken to mitigate the risk of corruption and ensure adequate levels of

integrity.

There were twenty

Ministries responsible for the 101 projects that were awarded via direct

negotiations, from May 2018 to February 2020. Of this, five Ministries had

projects worth more than RM100 million in total.

|

No.

|

Ministry

|

No. of

Contracts

|

Value (RM’m)

|

|

1

|

Ministry of

Transport

|

4

|

4,478.1

|

|

2

|

Ministry of

Defence

|

6

|

900.9

|

|

3

|

Ministry of

Home Affairs

|

8

|

517.7

|

|

4

|

Ministry of

Communications and Multimedia

|

12

|

380.1

|

|

5

|

Ministry of

Housing and Local Government

|

2

|

170.8

|

|

Total

|

6,447.30

|

The total of RM6.45 billion constitutes 97.6% of the grand total of RM6.61 billion in question. Two ministries – Home Affairs and Housing and Local Government – have Ministers in the present PN Government.

Under the

Ministry of Transport (“MOT”), the

single largest project was the Klang Valley Double Tracking (Phase II) worth

RM4.475 billion. This project constituted 68% of the total of RM6.61 billion

listed under direct negotiations. The double tracking contract was originally

awarded by BN and PH negotiated down the price from RM5.3 billion to RM4.5

billion, or a “savings” of about RM800 million. The shareholders include LTAT.

Surely this must have cleared the Cabinet of that time!

Then the Ministry of Defence

awarded Airod Sdn Bhd (“Airod”) contracts worth RM670 million. Airod is owned

by NADI Malaysia, which is the vehicle of MOF (and Tan Sri Ahmad Johan).

Others include Datasonic Technologies

(RM270.7m), TM (RM251.2m) and MYTV (RM254.5m) -- a Syed Mokhtar company which

had its original award in 2014. If it is a GLC or a MOF-owned, then the

taxpayer still benefits. Otherwise, one could allege perceptions of the wrong

kind.

Whatever the

case, it seems the boomerang launched by MOF is coming home to roost! Couldn’t

the Minister review the direct negotiations contracts done by PH and that of BN

and presented how respectable PN is compared to the earlier administrations?

Reference:

1. Direct Negotiations: Guidelines for

Managing Risks, Independent Commission Against Corruption, New South Wales,

August 2018

2. Siaran Media, Menteri Kewangan Malaysia,

26 August 2020

3. The Star, 27 August 2020

Thursday, 27 August 2020

In a Covid World: Growth or Value Stocks?

Apple,

Microsoft, and Amazon each have a market cap in excess of $1 trillion. Why? In

part because these companies have kept a steady eye on growth.

Meanwhile,

Warren Buffett, considered by many to be the greatest investor of our time, has

amassed a personal fortune of $73 billion. Why? Because he’s kept a steady eye

on value.

Growth

is typically defined by earnings per share (EPS) and sales per share (SPS).

High growth rates often drive higher “earnings multiples,” meaning investors

show a willingness to pay more per unit of current earnings, with the

expectation that growth should eventually “catch up,” so to speak.

How

do investors typically measure these so-called “multiples?”

·

Price-to-earnings

ratio (P/E). Basically,

this is a company’s stock price divided by earnings per share. It could be

based on the past 12 months’ earnings per share (“trailing P/E”) or on the

company’s projections (“forward P/E”).

·

Price-to-book

value ratio (P/BV or P/B).

This is the stock price divided by the stated value of its net assets (total

assets less intangible assets and liabilities).

Growth

stocks tend to show up in fast-growing industries like technology,

pharmaceuticals, and other modern industries. Think of “FAANG” stocks: Facebook

(FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Google parent Alphabet

(GOOGL). These are among the classic growth stocks of our day.

Conversely,

value stocks typically have low P/E and P/B ratios and lower expected growth

rates. Financial companies, automakers, and commodity producers are often

priced at low valuations, and thus get called “value stocks.”

If

you’re looking at individual stocks, consider looking first at the industry. Is

it associated with growth? Next, consider the P/E and P/B ratios. Here’s one

common rule used by some analysts: if the P/E is above 20, and/or the P/B is

above 3.0, it’s probably a growth stock.

As

bad as the pandemic has been, and as much as the economy has suffered, no

crisis lasts forever. This might give value a fighting chance versus growth as

the world emerges from this unprecedented period. The so-called “growth-value”

spread recently hit levels last seen two decades ago during the dot-com boom.

When spreads reached historic levels, it can often point to a change in the

weather.

The

chart shows only through December 2019, but the growth side continued to

accelerate in the first half of 2020 as FAANGs, biotechnology firms, and

semiconductors gained ground.

FIGURE: GROWING GROWTH? Over

long periods, both growth and value have had periods of outperformance. But in

recent years, growth has been the clear winner. Data source: MSCI.

Another way to track how they’ve performed differently, as

mentioned earlier, is to compare P/B ratios. About a decade ago, the average

P/B for growth stocks was around 4, versus around 1 for value stocks. Today,

P/B remains around 1 for value, but it’s zoomed up to around 8 for growth.

That’s the highest P/B for growth since 2000.

Growth likely benefited recently because so many investors

wanted large, familiar names that had weathered challenges like the 2008

recession and a 2015–16 “earnings recession.” But you could argue the move

reflected a scramble away from value as much as one toward growth.

As the economy reopens, people are getting back out again,

but growth stocks keep making new highs. COVID-19 is viewed by most economists

as a temporary shock to the economy. With many predicting improved conditions

in Q3 and beyond, will growth stocks continue their climb?

It’s a complicated picture, to say the least. Academic

financial gurus Eugene Fama and Kenneth French famously declared value (in the

form of low P/B ratios) to be one of the best factors for stock selection. But

their subsequent research suggested that growth factors of profitability and

reinvestment may be very similar in impact to value factors. It’s uncertain

which matters more statistically.

Believe

it or not, some of today’s steady dividend cash cows were once the upstart disruptors.

Consider IBM, which has a dividend yield of more than 5%. In the 1960s, IBM was

part of the “Nifty 50,” which also included stocks like General Electric (GE)

and Johnson & Johnson (JNJ). Those companies were arguably the Apple and

Tesla (TSLA) of their day.

So.

when it comes to choosing growth versus value, it’s hard to say definitively

which one is better. It may come down to your objectives:

·

Are

you looking for potential income?

·

What’s

your time horizon and risk tolerance?

Today’s

highflier may be tomorrow’s low-P/E, dividend-paying value stock. Plus,

investing doesn’t have to be an either-or, vanilla-or-chocolate, heads-or-tails

decision. Choosing a mix of growth stocks and value stocks can help you build a

diversified portfolio.

Reference:

1. Viraj Desai, Growth vs. Value Stocks:

Which Is Right for Right Now? https://tickertape.tdameritrade.com/

2.

Kelly

Bogdanova, Growth versus value investing in a Covid-19 world https://www.rbcwealthmanagement.com/

Wednesday, 26 August 2020

Malaysian Manufacturers Need Two Years for Business Recovery ?

The Star

Malaysian

manufacturers are pessimistic about their business recovery. Over two-thirds

need four months to two years to restore business to pre-Covid 19 levels. This

is based on sluggish growth projected globally.

Revenue and

profitability have been impacted negatively in the past 6 months. Only 8% enjoyed

higher revenue/ profit – and these were glove makers. About 46% of the

respondents in the survey done by FMM – MIER say they will cut down production.

Currently, they are operating at 50% of capacity.

About 42% of the

respondents are planning to cut costs by reducing up to 30% of workforce by

December 2020. Retrenchments will continue into 2021 albeit at a slower pace –

10% to 20%.

In terms of

business sustainability, about 34% of respondents believe their companies may

not survive beyond 12 months. Government support on wage subsidies and loan

moratorium are key to survival. The most vulnerable group, micro enterprises,

may need cash assistance. FMM suggested the loan moratorium period be extended

to December 2020. This will help with recovery and retention of workers.

The unemployment

rate is between 4.9% to 5.3% (for June/May) according to the Department of

Statistics, Malaysia. That suggests close to 800,000 people are unemployed.

More graduates will try to join the labour market and many will take a year or

more to find suitable employment.

The Government

has to address these issues – loan deferments, cash advances, employment – in a

practical one-year action plan if the economy is to achieve any semblance of

growth in 2021.

Reference:

1. Two-thirds of Malaysian manufacturers

need up to two years to return to pre-pandemic levels —

survey, 19 August 2020, The Edge

2. Almost half of manufacturers plan 30%

job cuts by year-end — FMM-MIER survey, 19 August 2020, The Edge

Tuesday, 25 August 2020

Covid-19: Four Airlines That Will Survive

Source: Rate a Cabin Crew

Some airlines are

going bankrupt. Many are selling or pledging their assets, doing their best to

survive the crisis. However, there are some airlines much stronger than we expected.

They are backed by extremely wealthy owners and ready to survive the pandemic.

Below are top 4 airlines that are well equipped to survive according to Amanda

Collins from rateacabincrew.com:

1. Chinese

Government Airlines – Air China, Chinese Eastern and Chinese Southern

These three

airlines are Government owned and plays a major role in expanding the influence

of China all over the world. Chinese government has trillions of dollars in

deployable capital and virtually unlimited options and reasons to keep these

airlines flying. Even if it takes several decades of operating at losses, the

owners of these airlines are well determined to keep them flying.

2. Qatar Airways

Qatar Airways is

owned by the Qatari government which has over $350 billion in known assets

worldwide. During the blockade imposed by Qatar’s neighbors several years ago,

Qatar Airways single handedly saved the country from starvation flying in

essentials including milk and bread from Turkey and Iran as well as dairy cows

from far off countries such as New Zealand. The airline flew aircraft even during the peak of the

pandemic crisis. A diverse fleet, superior product and access to virtually

unlimited funds makes Qatar Airways one the most resilient airlines to survive

the crisis.

3. Etihad Airways

Etihad Airways is

the flag carrier of UAE, owned by the Abu Dhabi royal family. Abu Dhabi royal

family owns Sovereign Wealth Fund and Investment companies Abu Dhabi Investment

Authority (ADIA) and Mubadala which has assets under management worth over $1

Trillion. Other major assets include ADNOC, the oil company owned by Abu Dhabi

government.

Etihad virtually

has access to any amount of money it needs. Etihad is also a strategic asset to

Abu Dhabi. Hence, no matter what, Etihad will keep flying.

4. Singapore

Airlines

Singapore

Airlines is owned by the Singapore government in the form of majority shares

and is a vital link to the Asian business hub. Without a national airline to

provide travel link to the country, the economy will collapse which makes the

Singapore government take a ‘whatever it takes’ approach to support the

airline. The government poured in over $8 billion in June 2020 to improve the

liquidity of the airline.

Some carriers like

Emirates are not on the list because the Governments do not have enough

resources to support the airline for an unlimited period. In US, all airlines

are public limited companies which put a limit on the cash it can access. The

major US airlines have tens of billions of dollars in liquidity but that can

last only for a certain period of time. If debt rises exponentially,

shareholders will lose confidence and will end up in insolvency.

Reference:

Amanda Collins, Top

4 Airlines That Will Survive the Covid-19 Crisis No Matter What https://www.rateacabincrew.com/

Monday, 24 August 2020

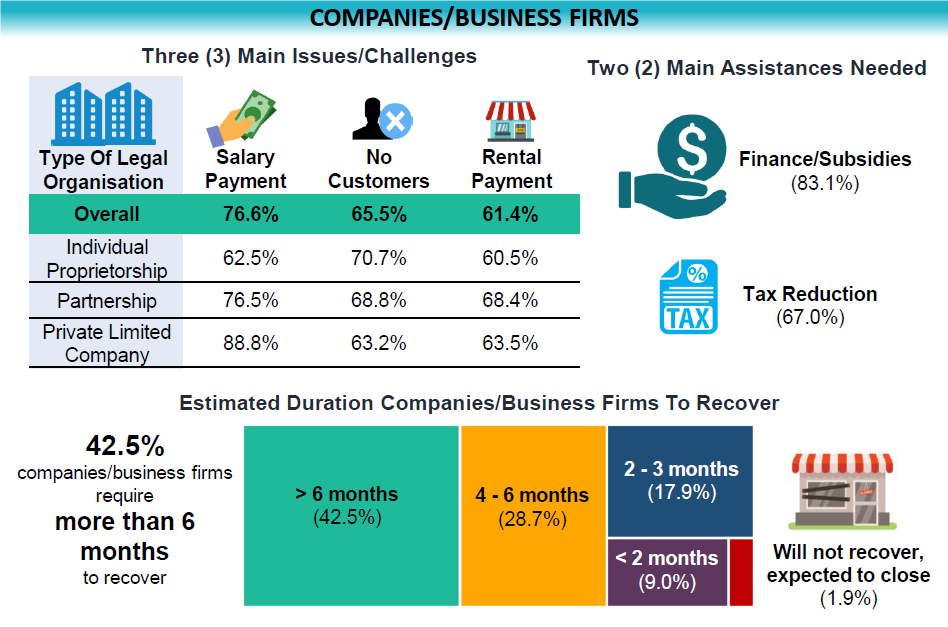

Effects of Covid-19 on the Malaysian Economy

The Department of Statistics Malaysia

undertook a special survey on the above. A total of 4,094 companies/firms

participated in the survey. The feedback includes qualitative opinion on the

effects of Covid-19 on the economy.

On Government’s incentives, surprisingly

over 34% were satisfied or very satisfied. Many (52.1%) perceive Prihatin

Package could ease their financial burden. That sounds as if recovery could be

soon. Is that true? What do you think?

Reference:

Special

Survey “Effects of Covid-19 on Economy and Companies/Business Firms”, Department

of Statistics Malaysia

Friday, 21 August 2020

Warren Buffet: Write Down Your Why

There are several reasons you might

decide to invest in a certain company. But Berkshire Hathaway CEO Warren

Buffett says there's one you should always avoid: Buying a stock merely because

you think it's going to increase in price. That's because even the best

investors aren't able to predict how the market will perform. Instead, you

should invest in companies that you both understand and believe will offer

long-term value, according to

Buffett. No matter how much or how little you're buying, you should

be able to get your reasoning down on paper without relying on outside

resources.

Source: https://www.moneycrashers.com

"Everybody when they buy a stock should

be able to take a yellow pad" and write down exactly why they plan to

invest in that company, Buffett said in a CNBC interview. Investors should not

worry about how the stock will perform in the near term. Buffett recommends

focusing on businesses that will hold their value over time.

Buffett follows three general rules when

deciding which companies to invest in: "First, they must earn good returns

on the net tangible capital required in their operation. Second, they must be

run by able and honest managers. Finally, they must be available at a sensible

price," he wrote in

his 2019 annual letter to Berkshire shareholders. That said, any

individual stock can over- or under-perform, and past returns do not predict

future results. Beginner investors are encouraged to look into low-cost index

funds instead, which are less risky.

Having said all that,

Covid-19 has punished Warren Buffet’s Berkshire Hathaway with USD9.8 billion

write-down due to Precision Castparts. Berkshire still has cash of USD146.6

billion and had just USD797 million in equities in second quarter (this is

excluding purchase of Dominion Energy for USD4 billion).

References:

1. Warren

Buffet Recommends a Simple Exercise Before You Buy Any Stock: Write Down Your

Why, Emmie

Martin, Feb 24, 2020 (www.cnbc.com)

2. Pandemic Punishes Warren Buffet as Berkshire Hathaway Takes Bid Writedown,

Reuters, August 9, 2020

Thursday, 20 August 2020

Working 40 Hours A Week: Is It Too Much?

Prosancons.com

“Eight hours

labour, eight hours recreation, eight hours rest,” Robert Owen, a Welsh

manufacturer and labour rights activist divided the day into three equal

eight-hour parts.

In the 1800s,

people in manufacturing worked nearly 100 hours per week. Today, 40-hour work

has been implemented in many developed countries (e.g. Europe, UK). In fact,

people working in Denmark, Sweden and Norway with fewer hours per week tend to

be more productive, happy and healthy. Even in Indonesia, the labour law

prescribes normal working hours as 40 hours per week. Meanwhile in Malaysia,

the Malaysian Employment Act defines the workweek as 48 hours, with a maximum

of eight working hours per day and six working days per week.

Working more than

40 hours a week benefit no one. A 2004 report published by the CDC’s Department

of Health and Human Services provides a summary of 52 applied psychology

studies on the impact of extended shifts and regular overtime. Across the

board, the studies found the impacts were negative—both for employers and

employees:

·

People

who regularly work overtime are less healthy. They’re more likely to gain

weight, fall ill, and get injured on the job.

·

People

are less alert and more likely to make mistakes after the 8th hour of work.

·

People

who routinely work extended hours and overtime are less productive.

Overwork can also

lead to sleep deprivation and stress. BNM's 2018 Annual Report stated that

higher labour productivity comes with higher wages and not by the duration of

working time.

But is 40 hours a

week still too much? The 40-hour workweek is rooted in industrialism. Modern advances in technology have

provided today’s workers with the tools to work anytime and anywhere. Therefore,

people can, and do continue working after they leave work for the day, check

their work email at night and even on weekends. On average, people work an

extra seven hours a week outside of the office. This makes us depend 100% fully

on our current job – our only source of income.

NEF (the New

Economic Foundation), an independent think-and-do tank in fact suggested a

radical change in 40 working hours to 21 hours. And 21 hours is close to the

average that people of working age in Britain spend in paid work. Moreover, it

could help address a range of urgent, interlinked problems: overwork,

unemployment, over-consumption, high carbon emissions, low well-being,

entrenched inequalities, and the lack of time to live sustainably, to care for

each other, and simply to enjoy life.

People today have

less time to enjoy their lives because the eight hours that they have each day

for fun are filled with chores and errands—more rote tasks to handle. This has

led some people to claim that the 40-hour workweek is too long.

There is still

not enough evidence yet to conclude either 40 hours or 21 hours is better for

an employee to work in a week. It depends on the nature and culture of an

organisation. But HR could consider the potential benefits of lesser working

hours when deciding the standard working hours of a company.

Reference:

1. Jessica Greene, Is 40 hours a week too

much? Here’s what history and science say https://www.atspoke.com/

2. NEF (2010), 21 hours - Why a shorter

working week can help us all to flourish in the 21st century

Wednesday, 19 August 2020

Are We Expecting a V-Shaped Recovery?

Malaysia’s

economy contracted by 17.1% in Q2 2020 – worse than the AFC in 1998. The Chief

Statistician of Malaysia says that in April, GDP contracted by 28.6%, in May it

was -19.5% and June had -3.2%. Slower contraction in June was observed in all sectors, except for manufacturing

and agriculture - both had growth of 4.5% and 11%, respectively.

Given the

contraction in April-June, the full year GDP is at best -3.5% to -5.5% in 2020.

The Malaysian economy is expected to stage a V-shaped recovery with growth

projected to be 5.5% to 8% in 2021.

The Department of

Statistics Malaysia has shown this in infographics as below:

Source: DoSM

The problem

starts after the moratorium period in September. This is when companies/ firms

need to meet debt obligations. Many are not ready for that! The optimistic view

from BCG is recovery beyond Q3 of 2021 while McKinsey projects Q3 of 2022. And if

one looks at IATA it is 2023 or beyond. Only businesses with deep financial

resources can survive. Most economists believe in a U-shape rather than a

V-shape. And some go on to suggest an L-shape. Whatever the alphabet, a vaccine

available will certainly shape-up matters.

Reference:

Bank Negara:

Worst is behind us, the Star, 15 August 2020

Malaysian Economy

contracted by 17.1%, worst since 1998, RinggitPlus, 15 August 2020

Tuesday, 18 August 2020

TikTok Sale: What Does Microsoft Want?

Bloomberg

The

artificial-intelligence software used in TikTok scans videos posted for

substance, form, and meaning, and uses that material to recommend more. You

don’t have to search for people you are interested and follow. Instead, you

download it, watch a few videos, and TikTok starts recommending more. And the

recommendations are surprisingly effective.

Trump has given

Microsoft 45 days (by September 15) to seal a TikTok deal. Microsoft might be

pursuing TikTok’s global operations, and Trump has signed an executive order to

block all U.S. transactions with ByteDance (and Tencent) starting September 20.

Microsoft’s

acquisition of TikTok may look unusual. Microsoft is about productivity, not

entertainment. Its experience with consumer businesses is mixed, the successful

stewardship of TikTok is not assured — think of the search engine Bing or the

takeover of Nokia’s smartphone business, both ended in failure.

Young people are

now growing up in an environment dominated by Android, iOS and Chromebooks in

classrooms. With Google Docs, it is possible to grow up without needing any

Microsoft software or services. TikTok gives Microsoft a connection to millions

of youngsters. Like how Microsoft used Xbox Live to fuel parts of the company’s

research for future projects. TikTok could help correct a Microsoft blind spot

and even change how its other software and services are developed.

The other tech

giants already have social data to train their AI algorithms on — Amazon has

Twitch, Google has YouTube, and Facebook has multiple social apps where users

post video content. A transformative Microsoft-TikTok tie up could help create

meaningful competitive position, leveraging other Microsoft brands like

LinkedIn, Minecraft and Xbox.

Microsoft once teamed

up with News Corporation and NBC Universal back in 2006 to launch its Soapbox

on MSN Video service. It failed against YouTube and was shut down a few years

later, leaving Microsoft to adopt YouTube as the primary way it shares its own

videos. Microsoft also experimented with its own social network, Socl, back in

2012 before shutting that down five years later. And now the company is

planning to acquire TikTok.

What do you

think? Is the acquisition worth the risk?

Reference:

1. What Would Microsoft Do With TikTok?

August 3, The New York Times

2. Emil Protalinski, ProBeat: Microsoft

wants TikTok for the same reason the U.S. fears China https://venturebeat.com/

Monday, 17 August 2020

“THE ROAD TO UNFREEDOM” Russia, Europe, America

We are living in dangerous times, Timothy Snyder argues forcefully and

eloquently in his book, “The Road to Unfreedom.” Leaders and followers, are

irresponsible, rejecting ideas that don’t fit our preconceptions, refusing

discussion and rejecting compromise. Worse, many are prepared to deny the

humanity and rights of others.

The road to

unfreedom, as Snyder sees it, is one that runs right over the Enlightenment

faith in reason and the reasonableness of others — the very underpinning, of western

institutions and values. Recent examples, found around the world, demonstrate

both how important conventions and mutual respect are as a way of maintaining

order and civility — and how easily and carelessly they can be smashed. Just

think of President Trump’s regular impugning of the loyalty of those who work

for the American government, CDC or the FBI.

So many in the

U.S. no longer care about understanding themselves and their pasts as complex

and ambiguous. Rather many look for comforting stories that claim to explain

where they came from and where they are going. Such stories relieve them of the

need to think and serve to create powerful identities. They also serve the

authoritarian leader who rides them to power.

Snyder makes a

valuable distinction between the narratives of inevitability and those of

eternity. The former are like Marxism or faith in the triumph of the free

market: They say that history is moving inexorably toward a clear end. The

latter do not see progress but an endless cycle of humiliation, death and

rebirth that repeats itself. Not surprisingly these often draw on powerful

religious iconography. Both, as Snyder points out, produce intolerance of those

who disagree.

Liberal

democracy is being undermined from within. In addition to the general malaise Snyder

identifies, “The Road to Unfreedom” also points to human agency — in particular

that of Vladimir Putin. At home and abroad Putin has willing collaborators and

“useful idiots,” as Lenin supposedly called them. Yet the evidence is that

Putin is ruthless in his determination to hang on to power and destroy those he

perceives as enemies of Russia, a large group.

He has used

covert and not so covert means (think of the “volunteers” in eastern Ukraine

who drove Russian Army trucks) to destabilize neighbouring governments and to

stir up dissent in countries from France to the United States. Within Russia,

as recent elections illustrate, he bends the Russian people to his will through

a mixture of coercion and persuasion. As Snyder says in one of his incisive

comments, Putin’s dominance is based on “lies so enormous that they could not

be doubted, because doubting them would mean doubting everything.”

To understand

Putin, Snyder argues persuasively that you must understand his ideas - a strange

and toxic mixture of fascism, religion and 19th-century notions about race and

the struggle for survival. His pronounced use of sexual imagery would also

interest Freud. There is a stress on power and virility and corresponding fears

of sexual nonconformity. Putin and his obedient press regularly attack gays and

gay rights as part of a Western conspiracy to destroy Russia.

So what can

the concerned citizen in the U.S. do about the decay in public life? As Snyder

says, keep digging for the facts and exposing falsehoods. As Thucydides, the

father of history, said, “Most people, in fact, will not take trouble in

finding out the truth, but are much more inclined to accept the first story

they hear.” Mistrust one-sided accounts of the past or the present. “The Road

to Unfreedom” is a good wake-up call. We may not agree with all of Snyder’s

conclusions, but he is right that understanding is empowerment.

Reference:

The

Road To Unfreedom, Russia, Europe and America, Timothy Synder, Tim Duggan Books

Subscribe to:

Posts (Atom)